Industrial metal prices hammered in May

Image: Kateryna Babaieva

TL;DR

A strong USD and anaemic Chinese production conspired to smash industrial and steel metal/mineral prices in May, again. Bulk prices decelerated by 13%. Bases decelerated by 5%. Why? Western interest rates remain high and the USD strong and while there are glimmers of potential real estate led stimulus in China, consumer wellbeing and geo-politics are keeping the Party occupied at the minute and no longer focused on construction/manufacturing. the industrial metals shakeout continues as we move closer to the next (lower) entry point.

Bulk commodities in May

Iron ore and the coal complex were matted in May. Prices decelerated 13% from April.

Base Metals in May

The world’s factory is open, but there’s less being manufactured. It’s also being starved of U.S. chip and other technology. Energy is expensive to import and populus wellbeing is now a key driver of whether the emperor gets to keep his lifetime clothes.

Price levels decelerated 5%, the biggest monthly price deceleration since September 2022.

Why Dollar?

The USD is strong and that makes commodities expensive to buy. It’s strong because U.S. interest rates are high and the dollar is in demand (to service USD denominated debt that continues to increase).

And as explained last week, there are 7 very good reasons for the Fed to continue hiking rates) and these are supported by Friday’s Jobs report for May which printed 339,000 non-payroll jobs and included 93,000 in upwards revisions for the previous two months. That means that Jobs were added at an average rate of 283,333 per over March to May. This is not signalling a slowdown, just yet.

Even if interest rates do not go up in June, more hikes are likely thereafter, and the dollar is likely to remain strong under either scenario.

Why China?

Xi is playing military and geo-political chess. He does not appear to be trying to break any manufacturing or construction records. Less civilian infrastructure and products are being completed. China’s post-lockdown growth impetus appears to have peaked. Any changes to this status quo will be as a result of stimulus and Party policy.

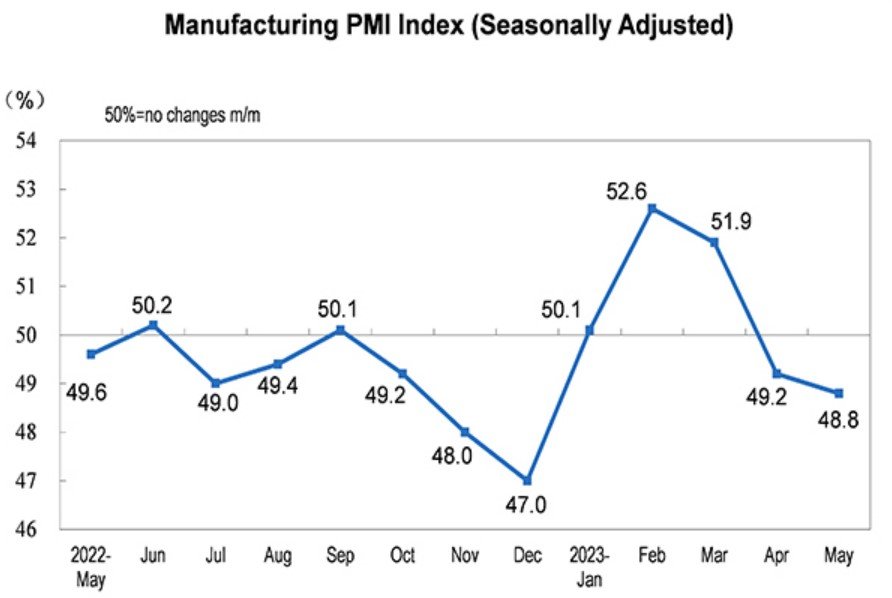

China’s metrics 👇👇👇

Source: National Bureau of Statistics of China

Source: National Bureau of Statistics of China

Live prices

In terms of live prices, Nickel and Zinc are continuing lower this month (June), with copper and aluminium stabilising a little, and while tin has bounced somewhat it does not appear to be powering back up.

Like last month, the industrial metals shakeout continues as we move closer to the next (lower) entry point.

See you in the market.

Mike

Image: Leonid Altman

Next Level Corporate Advisory is a leading Australian M&A, capital and corporate development advisor with a dealmaking track record spanning three decades. We help family, private and publicly owned companies build and realise value in their businesses, assets and investments.

All text is copyright NextLevelCorporate.