Did the Bond market finally hear the Hawk?

TL;DR

The short answer is that it heard the Fed’s call of ‘more rate hikes for longer’ and promptly faded it, again.

So I guess the real answer is, Nope.

The U.S. treasuries market still feels the Fed will be forced to pause, pivot and cut regardless of what Fed Chair Powell says, given a worsening economic outlook exacerbated by inflation, unhealed supply chains, Putin, rate hikes and liquidity withdrawal.

Hence, the longer end of the yield curve cratered as longer bonds rallied.

The tug of war continues as investors and traders alike speculate on when (not if) the Fed will change course.

Meanwhile, equity traders hear the Hawk and have punished loss making technology companies and price takers, but are still not ready to price in material earnings misses, just yet.

Refresher

On 5 December, I made the following comments after Fed Chair Powell’s ‘hawk dressed up as dove’ appearance at The Brooking Institution:

“Conclusion? More rate hikes to come, for longer, and based on his comments about exceeding the SEP levels, we’re probably going over 5% next year.

This is way more hawkish than dovish, right? And yet the market continues to front run a Powell Pivot and continues to fade his hawk.”

I also wrote:

“Plus, who’s to say even if it is 50bips on the 15th, that there aren’t more of them, i.e., 2 * 75 = 3 * 50 = 6 * 25...”

Powell did in fact opt for the lower 50 basis point hike. He also confirmed there would be more rate hikes and that he will keep going until the job is done.

Same but different; the action of the ECB’s Lagarde rhymed. As did the RBA and BoE, which also raised into recessionary sentiments.

Bonds

If we look to the red line in the chart below, we can see how the bond market reacted to the ‘slower pace but more of them’ vibe one day after the FOMC meeting.

Source:NextLevelCorporate chart, copyright

And while December’s curve so far is the most inverted we have seen since rates lift-off, if the market really heard Powell it should be pricing 3-to-6-month paper somewhere over the 5% mark, because that’s where the Fed says we’re going.

But alas, it only managed a minor upwards calibration at the short end.

What’s of more interest is the 2-to-20-year range where yields cratered. And even the 20 year cratered for the first time since rate lift-off.

Bond investors are taking positions in the longer end of the curve and pricing in a pause and pivot at the 6-month mark (call it May/June next year) as they see inflation and interest rates rolling over after that, and heading lower.

This suggests the market believes the Fed will (be forced to) start cutting rates in May/June next year.

U.S. Bond markets believe the Fed will be forced to pause, pivot and cut regardless of what Powell says given a worsening economic outlook exacerbated by rate hikes and liquidity withdrawal.

But it’s not just Powell being mister unpopular and intentionally tightening into a recession.

Over the past two weeks:

Lagarde of the ECB said more 50bp interest rate hikes for a ‘period of time’ and that the ECB was not "pivoting" yet, even in the face of almost certain recession.

Bank of England said it will continue to respond ‘forcefully’ if needed after also raising 50bp (now at 3.5%).

RBA raised by 25bp to 3.1%, a full 300 bp up from 0.10% in April.

Whereas China is stimulating and the Bank of Japan continues to:

give away money to try and stimulate real growth through yield curve control (YCC), although there was a slight increase in the YCC band around the zero bound from + or - 0.25% to + or - 0.50% (which could signal a slowdown in loosening to avoid irreversible damage to the JGB market which appears to be fundamentally broken).

purchase a necessary amount of Japanese government bonds (JGBs) without setting an upper limit so that 10-year JGB yields will remain at around zero percent.

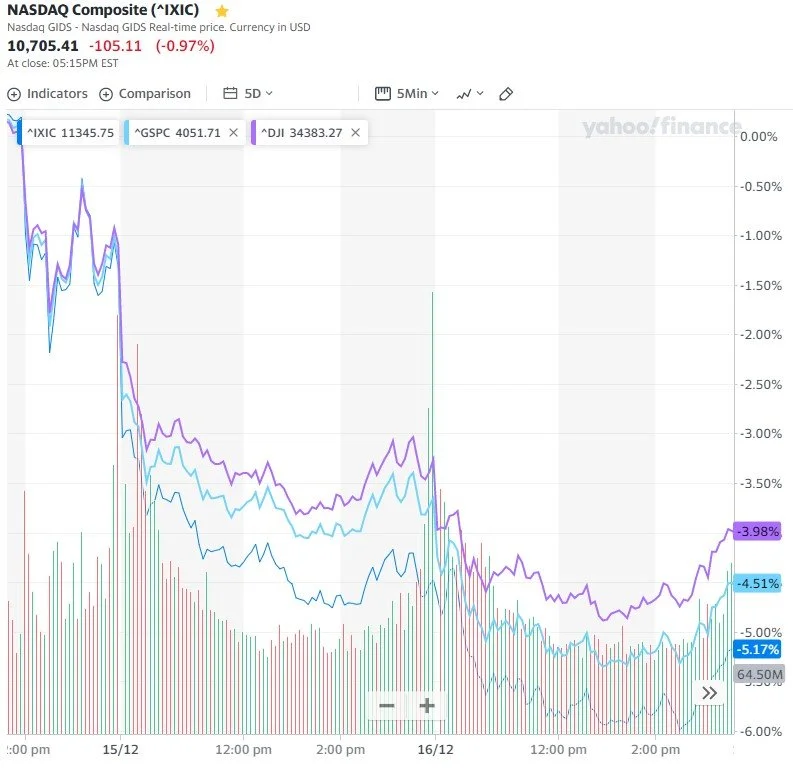

Equities

But equities heard the hawk, again. They listened while traders pulled splinters from their chests, particularly in the low/no profit sector of the market that’s sensitive to interest rates.

And it also occurred in the value end with fears of upcoming earnings shocks becoming stronger.

But no panic just yet, just some people in the brace position.

European stocks were down by around 3.2% after Lagarde’s ‘no pivot to see here, folks’ speech.

And on ASX, many sectors were belted, including some bulk metal stocks as the China centralised buying strategy via CMRG floated into the traditional media.

More recently, woke metals have taken a hammering.

So, is the fade starting to fade?

Maybe a little in equities which are starting to price in lower earnings.

But bond markets continue to fade/front run central banks on the assumption that central banks will not be able to continue with rate hikes as forcefully and for as long as central bankers are saying, and instead will be forced to pause, pivot and cut in the near-term. That’s why gold and silver and long end bonds have been on the move.

Still, Powell continues to say he won’t stop the tightening prematurely for fear of having to invoke a real Volcker tightening.

Happy Holidays, see you next year!

Mike