China dependence, COVID and India

COVID is cyclical, but the rise of China and our dependence is secular.

Secular, or long term trends have a habit of trickling down and creating cyclical (short term) dislocations in economies and markets.

That can be important for your business, and the businesses owned by the companies in your investment portfolio. Worth taking notice, right?

Even though it’s been devastatingly endemic in many countries, COVID is a cyclical event and subject to vaccines working we will get past it and become better equipped to tackle the next pandemic in a more measured way.

That’s why I was happy to read an article in the Fin Review which reported that Australia’s best CEOs had put COVID into context (economically) by saying that regional risks and challenges associated with our dependency on China, is a bigger issue than COVID.

Yes, China dependency rightly or wrongly is way bigger and existed way before COVID came to town, and our economic positioning (and direction of our currency and trade balance) is best seen in light of this and other often connected secular themes.

Here, we are fortunate to be delivering record quantities of iron ore to China as a result of: (a) increased demand due to China’s construction-led COVID recovery plan; and (b) Brazil iron ore supply chain blockages as a result of both environmental disasters and COVID.

But in as much as this endowment income has carried the country through COVID, it has only worked because of the Chinese Communist Party’s requirements, and like no other time before this has exposed Australia as a highly dependent supplier to, and buyer from the middle kingdom.

And, the interplay of China’s rise to an at least equal hegemon to our strategic allies means that we are caught in a hard to digest geopolitical sandwich.

Can you hear the whispers?

No, they could not hear the whispers all those years ago.

And since then, China awoke and modernised and the West wanted access to the land of a billion (future) consumers. Withdrawing from the Vietnam War was the price.

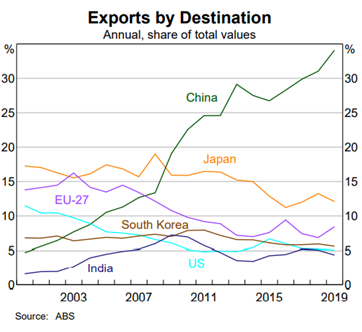

Assessing that deal 50 years after, i.e., today, we see that non-China now has more or less access to 400 million middleclass consumers, and Australia has become economically dependent on China.

To understand why this dependency is now risker than ever before (and COVID) we need to carefully listen to the super narratives shaping Australia 2.0, and then imagine how they will express themselves in our trade balance and currency - depending on whether we can develop a common conviction within the region. But more on that later.

Here are the key movers and shapers of Australia 2.0.

The 50 year making of Modern China and its challenge to the hegemony of our key economic and military ally, the U.S.

Quantitative easing in however much and for however long is required (QE Infinity) which is a train to monetary nowhere that the U.S. Federal Reserve (the Fed) and the European Central Bank do not know how to stop, and which has pinned U.S. short rates at zero.

No ‘growth fiscal’ to speak of just yet due not only to shutdowns, but also the Fiscal plumbing that seized up for most governments as a result of the popularity and ease of pumping up secular 2.

Crumbling value of fiat currency in a net price disinflationary world resulting from technology and a non-spending ageing population.

Multi-speed economic performance (and currency pair gyrations) caused by dislocated supply chains (creating some inflationary winners and some service based losers), shifting comparative advantages as a result of technology, and trade warring in response to secular 1.

A shift to renewables and green personal transport which on one hand hurts coal and oil, but on the other supports EV and renewable metals like rare earth elements, silver, and EV minerals lithium, cobalt, copper and nickel, all of which Australia can play a big role in.

Australia’s critical position in China’s weaponised supply chain for iron ore, renewable/EV minerals for permanent magnets and batteries, and many of our soft commodities, means we have this dependency on one export customer that is also Australia’s number one source of cheap imports, but which are probably net disinflationary.

Seculars 6 and 7 are the most pertinent because China exports make up 1/3rd of Australia’s export income, and if that disappeared the Aussie dollar would literally collapse. In turn, that would make cheap imports more expensive and we would import price inflation.

So, if Australia was a company, Josh Frydenberg could expect to receive a qualified audit report and a ‘review event’ letter from the bank.

COVID-19 as a pandemic/endemic will pass once vaccines are in arms and doing their job over the next few years, and maybe a new one will come in time, but I’m afraid this fire breathing dependency will be around for a lot longer.

Enter the dragon.

One big export dwarfs all others (hint: it’s on the left).

Note the left hand axis is on a different scale

One massive dragon egg in our export basket.

Our number one customer has returned to pre-COVID levels, but no other country has.

Even with more financial support, China corporate yields and inflation expectations have been rising, not falling.

At present, the AUD like many other currencies has strengthened against the US dollar, so Aussie iron ore exporters receive less AUD for their sales (and expend more valuable AUD on the bulk of their domestic cost base - and even moreso when there are cost overruns at replacement mines).

Employment in our services industries has gone Wile E. Coyote and is nowhere near to recovering. That’s a vaccine and unlock story.

From a share of output perspective, mining has doubled in a short time frame and is now carrying services and everything else. Wait till you see the FMG dividend.

Drilling down into mining, and also counteracting the Aussie Dollar’s strength against the USD has been a massive increase in volumes sold, and prices, particularly for iron ore.

Up to date spot price increases are not reflected above, but they are baked into the chart below.

And to really see them we need to separate out the spot iron ore price and denominate it in SDR terms (SDR terms remove changes in any one currency, i.e., in this case remove the effect of the AUD which continues to strengthen while the USD weakens due to QE Infinity and lockdowns). In SDR terms, iron ore and coal prices together increased at a blistering:

22% in December 2020

44% over the past year

These are massive increases in spot prices and even moreso for iron ore when you consider coal prices decreased over the year, and are a function of:

curtailed Brazilian ore supply due to dam and environmental disasters as well as COVID

increasing steel input demand to feed China’s construction and infrastructure project-led COVID recovery package

no alternative supply sources at volume, yet, but see next section

no long term contractual pricing mechanisms

In summary, a stronger AUD (weaker USD) counteracted by increased prices and volumes due to Brazil, COVID and a fast recovering China that can’t replace 700 million tonnes of iron ore inputs overnight, means super high prices for Aussie iron ore exporters and unexpectedly large royalty income for the moment.

Dependent? Yes!

So what?

Well that’s not hard. Prices tend to revert back to the average or mean, particularly when cycles change.

With 20% of iron ore sourced internally and a goal of replacing 20% of its current iron ore imports with ore from accelerated investments and other ventures (not Australian ore) - China is heading for 40% self-sourcing and increased pricing positioning.

It will take time though, and that should give us time.

To do nothing and remain dependent on one customer until it’s too late, is risky.

Some hard questions for Australians.

In the interim, should WA iron ore producers come to the party with alternative pricing mechanisms to help settle tensions and relieve tariffs and imposts on other Australian exports (coal, barley, meat, etc) or will business look to other markets, like the crayfish industry?

Capitulating on price does not remove reliance. Developing new markets does.

Are China tariffs punishment for backing the Trump administration’s call for a COVID enquiry, or is it an inevitable sign of Chinese hegemony and wanting to take the pricing power out of the Pilbara?

Even the Biden camp looks like it will go hard on China. Will Australia take an opposing view to neutralise tariffs, sit on the fence, or dish out more of the same?

Is there a bifurcation between strategically oriented business leaders and governments, in the way that they are viewing our role in the geopolitical sandwich? Probably. Yes.

What about the new incremental iron ore projects that are springing to life? If China demand continues they might be OK and make money. If not, they will become toast just like Atlas Iron was the last time around, and this time some won’t be lucky enough to be bailed out.

But governments would be very happy with WA at the moment, in spite of the dependency.

WA leads the country because of the commodity boom (mainly iron ore) and you can see that WA’s orange line, which I often write about, is well above the two non-commodity states of NSW and Vic where most of the country’s population lives.

Yup, back to boomonomics when WA carries the nation.

And then what happens if and when China replaces enough of its iron ore imports such that it can start to exert pricing pressure on the Pilbara?

Or when China retaliates with more tariffs on more Australian exports because it can’t replace Aussie iron ore quick enough for its own tastes?

Is China’s direct or indirect ownership of our endowment (with our iron ore and soft commodity companies taking a clip on the way through) good for Australians, and the world, in the long run?

With strict foreign inbound investment rules and the old faithful carry trade between Australia and the U.S. gone, don’t we need to find a better way to coexist in the region with our neighbours without selling the farm and without blowing up our strategic alliances?

No more carry trade.

China is not the only regional player with needs.

I’ve heard people ask how one should feel about exporting iron ore one day, and the next day importing steel back from China in the form of bullets and weaponry.

Is that unsubstantiated fear and/or racism, or is it a matter of homeland security. What do you think?

What about a Chinese city on PNG? Too close for comfort? Too far to care?

OK, so everyone will have a view, but while we are thinking about this there is another sleeping giant in the region that could use our help.

Why does an Indian steel industry using Australian iron ore sound so foreign to people? Is it racism, or just short term thinking.

India shares our status as a Commonwealth country and its proximity is compelling for shipping materials. Around 20% of the world lives there and it has a super young population, with an average age of around 30 years. That population wants a better standard of living.

Developing bilateral industries (iron ore, steel, education, agribusiness, etc) would certainly be value creative and provide competitive pricing tension in the region, and Australia and India are very old friends. Helping India to increase GDP into something more befitting what its population would suggest is worth a thought. Funding, technology and bilateral industries and education would be the key drivers of this, but India cannot do it alone.

Perhaps Australia, the UK and the U.S. would be similarly interested in assisting India in ways that do not put our economic interests at odds with our strategic interests. It’s probably no secret that this would help neutralise the soft power that China has been seeking to enforce in India through its Belt and Road initiative.

Still, short termism, supply-side greed, exclusive ideologies, racism, fear and other factors are driving irrational behaviours and missed opportunities (for all sides), and all facets need to be understood and debated before we can arrive at a common conviction.

Whichever way we go, I like to keep Henry Kissinger’s warning in mind:

“The challenge to both sides is to see whether we can develop enough of a common conviction about the future, so that we can spare the world a conflict between two great societies." Henry Kissinger, 14 November 2019.

What’s sure is that we sit on a massive mineral endowment situated in the middle of a U.S./Sino geopolitical sandwich. There is much potential to use this for the benefit of the region, and without newting the next generations by selling off our farm. But, what we do about adding value to this endowment and with whom and which neighbours, will define whether we set ourselves up for a sustainably bright future, or we get used to chewing on bananas well after COVID has passed.

Stay safe.

Mike

Next Level Corporate Advisory is a leading M&A, capital markets and strategy advisor with a multi-decade track record of delivering high quality independent corporate advice and strategic transactions. We design, find and arrange transformative mergers, acquisitions, divestments, IPOs, growth financings and other corporate events that help our clients take their operational and corporate strategies to the next level, in and out of Australia.

All text in this article is copyright NextLevelCorporate.