Fed hits $8.5 trillion and Kirk goes to space

Image: Lisa Fotios

Life imitating art.

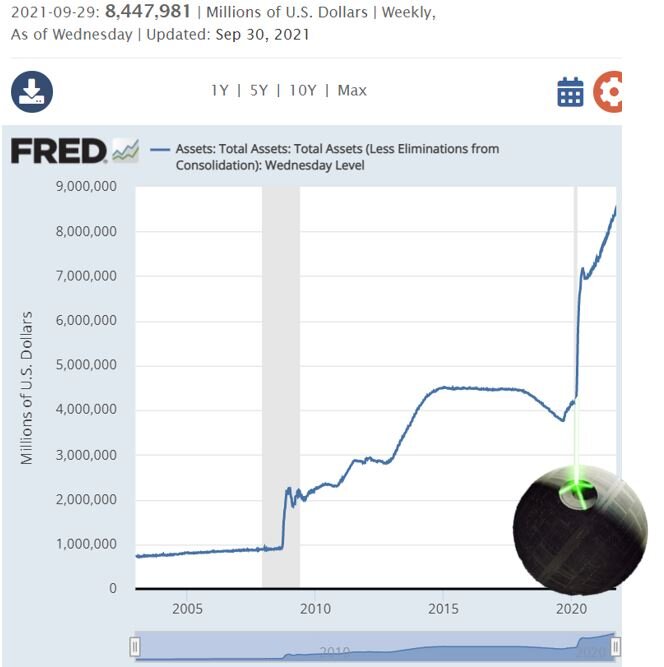

If I said to you a few years ago that the Fed’s balance would hit $8.5 trillion (oh wait, I did) and that Captain Kirk was real, you would have laughed at me.

So with equal parts of awe and amusement, today we hear that William Shatner is about to head for space in Bezos’ Blue Origin 🚀🚀🚀🚀🚀 and while that means he really does get to be Captain Kirk (and Blue Origin gets a once in a lifetime advertising dream) it’s nowhere near as stellar as the current record size of the Fed’s balance sheet that just hit $8.5 trillion (minus change).

That’s not so good.

A forever growing Fed balance sheet is not good because as a proxy for ‘dollar money’ each time it grows the dollar debases and it takes more dollars to buy the same, if not cheaper goods and services.

It also means that treasury and bond markets become fake as a result of the Fed being able to control the level and shape of the yield curve (i.e., the cost of money at various maturities).

So, what of the Fed’s attempt to slow this down with its much touted taper?

First, what’s a taper?

A balance sheet taper rolls on the basis that instead of buying the current $120 billion per month in treasuries and securities, FOMC (the trading desk of the Fed’s open market committee) would only purchase say $110 billion, and then $100 billion per month, and so on and so forth - i.e., it effectively taps on the brakes.

Second, is it real and will it be meaningful?

Yes, the Fed thinks it is, and probably no, it won’t be meaningful.

I’ve suggested for some time now that if a taper is implemented, it’s unlikely to be meaningful or long.

Why?

The Fed’s growth forecasts look over-cooked particularly in light of fiscal (welfare) stimulus being removed next year and slowing growth in China and Europe.

The difficulties Democrats are having in getting the debt ceiling raised (due in two weeks) which will probably mean that Biden will be lucky to keep the Government open and avert a default if he winds back his rich demands.

The oil shortage will tranquilize open economies, and level-up costs for all construction, mining, materials, transport, cyclicals, etc., as well as erode disposable household income.

Most of the productivity increase in Industry 4.0 will come from software and machines, not from people, and with people leaving the workforce because of this and/or a reassessment of work/life and health balance after COVID, and/or because they are retiring boomers, there is likely to remain a large swathe of unemployed,

Notwithstanding those for factors, let’s assume the Fed tapers from November.

Theory: If there is an ‘opening up’ next year and the oil/energy shortage continues, with the added drag of higher interest rates, machine versus people productivity, and the assumption that Fiscal stimulus has been removed, there is a high probability the Fed would need to stimulate again, i.e., stop the taper and buy more paper to keep rates down and avoid a major correction in equities (and damage to the collateral base).

That’s why I think a taper won’t be meaningful, or long lasting.

In the meantime?

Equities are likely to face headwinds as the market braces for a taper, a thorny debt ceiling negotiation, and Evergrande, as well as no more fiscal stimulus next year.

The probability starts to increase for more QE as opposed to tapering.

In other words, the Fed has to do the heavy lifting again, and that’s why I think there is a credible chance the balance sheet might continue to grow in the long term, as opposed to shrink.

I’ll be the first to say that it appears the Fed is betting against the above scenario, and we know this because it’s forecasting 5.9% growth this year (which means there needs to be a shed load of growth in the next 3 months??) and 3.8% for next year. That’s pretty huge.

The market also seems to believe the Fed, and that’s reflected in bond yield action.

If the Fed is wrong, NASDAQ and high PE stocks crater, value stocks go sideways, the Fed stimulates again, yields are managed down and we see a very strong USD, together with capital flight from emerging markets and difficulty in raising money for cyclicals.

Of course in the long term, and with the energy transition ‘on’ the theory that cyclical metals become more of a secular story probably has merit, so for those of us with a long term view, this would be a speed hump.

For others, it would be something more.

Hard to see the gravity, when so big and heavy the balance sheet is.

Mike.

Next Level Corporate Advisory is a leading M&A and capital markets advisor with a 20 year track record of delivering the highest quality of independent financial advice as well as strategic transactions to help our clients level-up.

All text in this article is copyright NextLevelCorporate.