Eyes on Powell as key catalyst for equities, after Brexit and China tariffs cool

Last minute progress.

Progress was made last week by Donald Trump and Boris Johnson on their respective Nationalistic agendas, in the lead up to the northern winter break.

The U.S. and China.

Last Friday in the US, December 15 tariffs on the balance of imported Chinese goods were shelved, with the retaliatory Chinese tariffs on US corn, wheat and auto imports cancelled on Sunday.

So far under the preliminary deal, the original 25% 301 tariffs will remain, and the 15% tariffs will be reduced to 7.5%, with IP protection, technology transfer and other key issues also addressed.

But, it’s premature to celebrate given the 86 page detailed agreement has not been made public nor signed (expected to be in January) and a phase two deal and a process to get there are yet to be agreed by the parties.

There’s also the question about how hard the US will push China to unwind its corporate subsidies model, which creates a competitive price advantage when Chinese firms compete outside China. That may not be so easy to unwind.

For the moment, both leaders have agreed a ceasefire, signalling that a de-escalation is a good way forward, and at a minimum the stop-gap phase one understanding will avoid the damage that the December tariffs would have brought.

Here’s the phase one deal fact sheet from the Office of the US Trade Representative. It’s not the English translated 86 page version that is yet to be signed, so don’t be surprised if things are different in January.

A big win? Not really, not yet.

The U.K.

Similarly, in the UK voters delivered Boris Johnson a large majority of 74-75 seats in the House of Commons, with Brexit now almost assured given the next election isn’t until 2024 and labour is in tatters (sounds familiar). That said, the time for celebration is also premature in the UK given there is much work to be done to ratify it and then avoid the remaining possibility of the UK crashing out of the EU without a deal next year. Assuming the Withdrawal agreement gets ratified swiftly, a 11-12 month timetable to negotiate the trade deal/s is tight, to say the least.

Nonetheless, both of these ceasefires have lifted equities markets and optimism.

Will there be roll-backs, back flips and cultural differences of interpretation? Probably, but the market works on sentiment and these somewhat opaque events are providing a nice dose of optimistic inertia.

Tonight as I write there is an avalanche of “xyz reached a 52 week high” or in the case of Apple, “AAPL reached an all time high of $278.06”.

Optimistic, yes, but Powell is driving equities.

Optimism, yes, but the key catalyst for equity markets to continue their stampede, in the absence of a European financial crisis, a US impeachment, war, or an existential climate threat or similar, is Jerome Powell.

US Fed Chair Powell has moved the American economy into Goldilocks territory by utilising three mid-cycle adjustments to produce a not too hot, not too cold economy, with evidence including a strong non-farm payroll increase of 266,000 jobs in November, albeit with the full year average only at 180,000 which is still considered to be too low.

Add to that, no real catalyst for a material inflationary breakout.

This is affording the Fed an ability to park interest rates where they are for the time being. There are even 4 members of FOMC who are predicting higher interest rates next year. Many can’t see that just yet. However, if there really is a phase one trade deal with China with meaningful content (yet to be seen) and progress with a detailed phase two agreement and a ratified Brexit Withdrawal agreement, this may be enough to provide some impetus for global GDP to wake up, a little.

Had the trade war not occurred, perhaps Powell would not have had to introduce the mid-cycle interest rate adjustments. Nonetheless, we can say that Powell reacted to the data, if not the President’s jawboning.

If the so-called ‘trade deal’ turns out to be smoke and mirrors, he has a little bit of room to move down the curve before having to flirt with negative interest rates.

Which corporate finance windows are likely to open wider in 2020?

It is likely that the IPO window will creak open a little more, and corporate M&A transactions funded by premium equity prices and almost free money, will likely increase (note the recent all cash splurge by LVMH for Tiffany’s).

With low and accommodative monetary policy as it is, businesses which feel a little more confident will no doubt chase cheap money to buy market share, in the absence of inflationary growth.

What’s also of interest to me is that multiples are likely to become more demanding, before they settle down. Reasons:

Equities are still the most preferred investment class and this is causing upwards pressure on prices, particularly now the market has started to flirt with optimism.

There may be some time before the perception of higher earnings growth in the event of a real trade deal gets baked into earnings forecasts, i.e., the market needs to see the detail and event then there will be a lag before the E closes the gap with the P.

In light of this, in 2020 I think we will see more:

Companies seeking to raise cheap capital for organic growth and/or buy-backs, further fueling prices.

Companies seeking to raise cheap capital for acquisitions to buy market share (in the absence of inflationary growth).

Baby boomers looking to sell out at seemingly increasing multiples.

VC and Private Equity investors ready to exit.

Assuming no imminent threat of war or inflation and assuming low interest rates for longer, it is likely this will create a floor under the gold price. Oil is likely to make a comeback as well.

Impeachment of PROTUS?

Johnson, Nixon (who resigned before being impeached) and Clinton had to face it - and now Trump?

No point in speculating, but even if this was to occur it is unlikely to have a lasting impact on equities whilst interest rates remain low and in the absence of the kind of tear-away inflation which is unlikely to occur in the short term.

Japan, China and Europe.

More monetary stimulus is almost guaranteed for these economies. But, 2020 needs to be the year for fiscal stimulus as well. In Europe in particular, we are waiting to see how persuasive new ECB President Lagarde will be in getting various EU members to accelerate fiscal measures, or to develop some sort of fiscal instrument to cushion the next crisis.

If there is some meaningful and sustainable impact from the phase one trade deal (if it gets signed) and if the phase two deal addresses the remaining issues; and in the UK if the Withdrawal agreement is ratified and progress is made on trade negotiations, there may be some fairly decent tailwinds to encourage sensible fiscal stimulus in key economies.

All of this is yet to play out, starting in January.

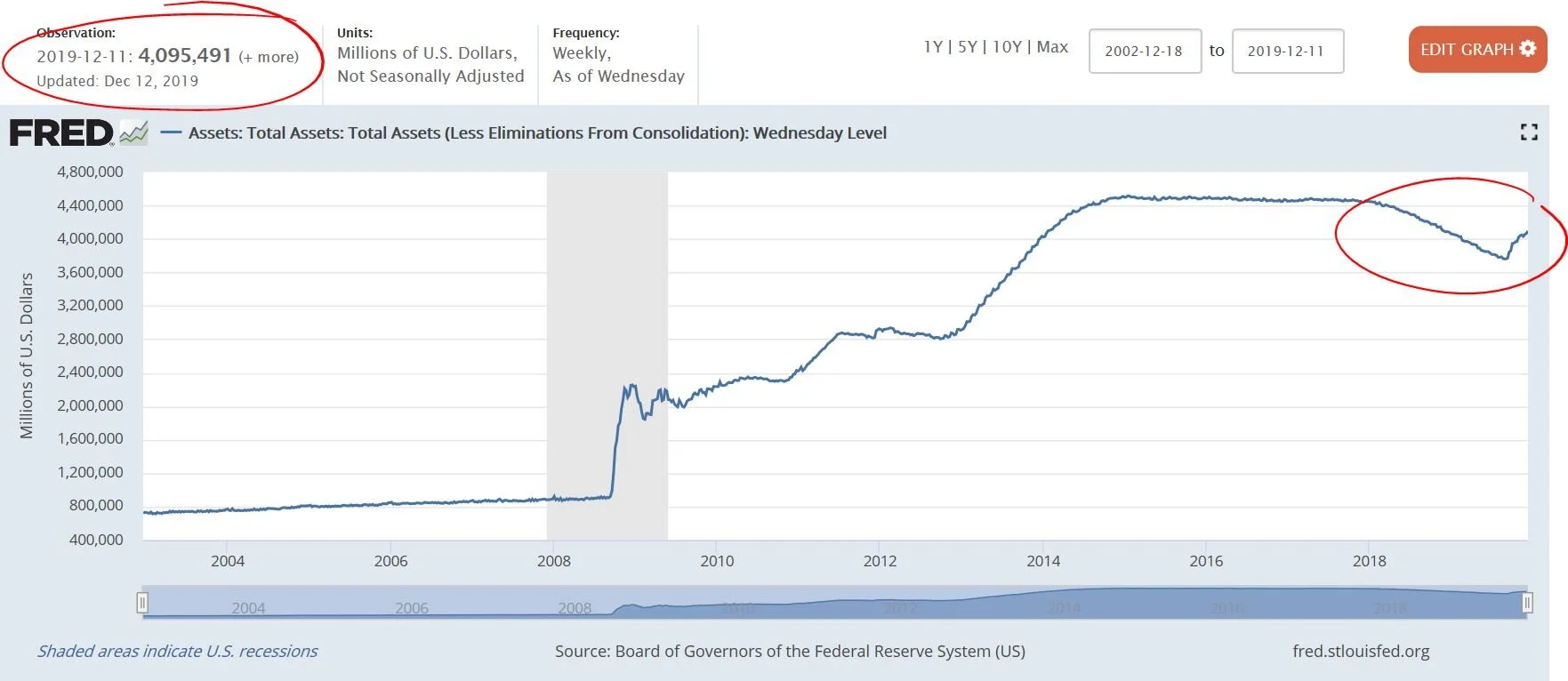

Watch the Fed’s balance sheet in 2020.

However, the tell-tale sign for a reversal of this optimism (apart from a trade deal back flip and/or EU Withdrawal agreement hiccup) will be a continuation of the US Fed’s balance sheet expansion - and that of other central banks.

In October the US Fed started monthly Treasury purchases (at a rate of US$60 billion per month) in an attempt to supply more liquidity into markets to keep a lid on repurchase interest rates.

Powell said it was in no way QE. I’m not so sure. What’s more - when Powell tried to drain the U.S. great lakes of their US$4.5 trillion in free money (continuing Janet Yellen’s run-off) he was unable to get below US$3.7 trillion before topping it back up to US$4.1 trillion, where it stands today.

If this continues at the same rate, it will be a sign that even 11 years after the GFC the US economy is insufficiently resilient to drain the lakes, and corporate earnings expectations will be impacted.

Finally, here are the Fed’s GDP projections, looking forward from Q3.

Perhaps these forecasts will be revised as more information comes to hand on the phased trade deals, Brexit progress and other trade fronts which have opened up, e.g., US retaliatory tariffs aimed at (and bizarrely sanctioned by) the EU in response to the Airbus subsidies, and which I wrote about in September.

For that matter, it’s best to keep an eye on the 4 key central bank balance sheets (US Fed, BoJ, PBOC and ECB) which currently sit at ~US$19.7 trillion combined, with around 75% being negative interest rate paper.

Mike.

NextLevelCorporate is a leading financial & strategic Corporate Advisory firm with a multi-decade track record which speaks for itself. Helping clients in all industries to prepare for, respond to and deliver transformative M&A, Growth Financings and other corporate finance strategies and transactions in and out of Australia, is our passion.