Amazon might be facing solid competition, but they have to face Amazon.

Source: Bloomberg.

I don't know about you, but I certainly would not want to be taking on Amazon, right at the moment.

Amazon's quest for global domination means that it will sacrifice profits for market share in existing and new markets and consumer verticals, whether that be retail, products, cloud services or anything else.

The objective? Improve the customer experience for more and more customers and then feed more products and services into the massive and omnipresent Amazon pipe.

So, spare a thought for those who are late to the online retail party and are not a logical 'millennial' destination platform - Walmart being a great example.

Walmart has been attempting to tap into millennials via a reverse Amazon/Whole Foods strategy, i.e., starting with 'bricks' and adding the 'clicks'.

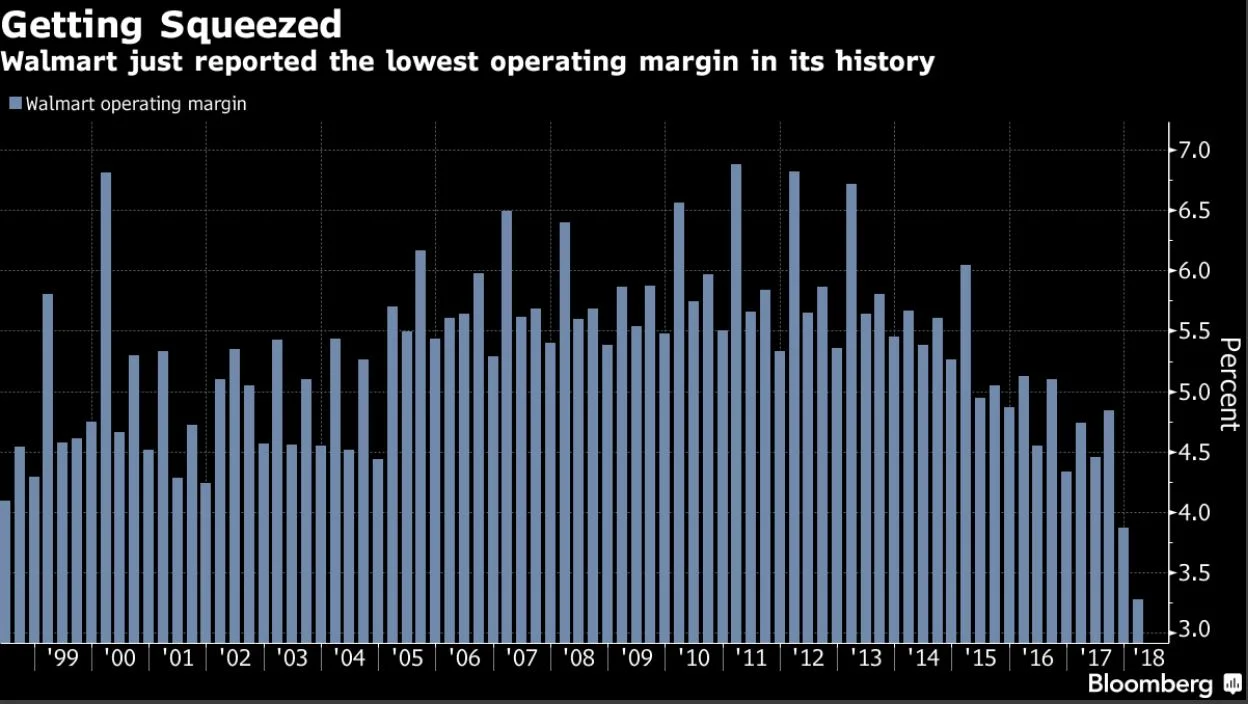

However, Walmart's recent results indicate a record low operating margin of 3.3% as per the chart above, uh oh, plus a big drag on performance as a result of re-investment in e-commerce, just to catch up.

One school of thought is that Walmart will need to spend a lot more on reinventing itself organically and through acquisitions like Jet.com, into a destination for the online consumers - that however is a big bet even for Walmart, and will continue to weigh on profits.

Take a look at this Bloomberg article which nicely captures the conundrum.

These high stakes bets are similar to those being made in the online entertainment/streaming sector.

In August last year I wrote about Netflix committing to spend US$15.7 Billion on content to protect its advantage, and in December I noted in 'Murdoch's Dump is Disney's Pump' the US$57 Billion sale of the 21st Century Fox Hollywood assets into Disney.

The assets include a 30% interest in Hulu which when added to Disney's existing stake provide it with control and logically allow Disney to re-house its streaming content after withdrawing it from Netflix.

No doubt these high stake business reinventions will continue in order to survive and to one day build a quantifiable competitive advantage.

Who will come out with the advantage is still up for grabs, but it will come at a massive cost. If inflation really is back and if interest rates are again on the rise, at least in the US, it will come at an even greater cost.

Mike

NextLevelCorporate delivers independent and transformative corporate advisory and financing solutions to clients looking to reshape their competitive landscapes, in and out of Australia. Our ability to do this comes from ~30 years of sector-specific proprietary intel and the freedom to independently originate and advise on customised Mergers and Acquisitions, Growth Capital and Special Situation investments.

You can subscribe to our newsletter here.